Bust-up Credit Card Monopolies

End Usury Preying on Americans

American household debt increased to $17.94 trillion in the third quarter of 2024, according to the Federal Reserve Bank of New York. This includes major purchases such as a home (mortgage) and an auto. Shockingly, $1 of every $15 of debt is from credit card balances. Americans set a new record for credit card debt at $1.17 trillion last quarter.

This matters because unlike mortgages or auto loans that carry average interest rates of 6.9% (for a 30-year fixed rate) and 5.25%, respectively, credit card customers could be charged an annual percentage rate (APR) as high as 34.99%.

This is the free-market at work, right? No. The free-market is virtually non-existent in today’s credit card universe.

First, let’s review today’s use of credit cards. Credit cards are indispensable in this day and age. This is especially true in the business world. Large or recurring expenditures such as travel, business purchases or entertainment require a credit card. For business expenses, someone can charge a cost, get company reimbursement, and pay the bill when it comes due. While useful, debit cards are limited to the amount that is in an individual’s bank account.

One of the many outcomes of the Covid-19 pandemic was the increased use of credit cards by typical Americans to make payments as public authorities and businesses encouraged the public to engage in contactless payments. This came at the expense of using cash. The credit card share of all purchases increased from 18% to 31% between 2016 and 2022. The use of cash fell by the same percentages (31% to 18%) during the same period. The use of other payment methods such as debit cards and digital wallets remained unchanged.

Credit cards are not being used solely to purchase new appliances or high-value electronics. Today, nearly one-third of all grocery purchases are made with a credit card. The rate is nearly identical for restaurant purchases. 80% of consumers who use a credit card to purchase groceries do so to better manage their finances, according to spending and payments analytics firm PYMNTS. Nearly one-third (31.2%) of shoppers report using a credit card is the only way they can afford groceries. Add to this the staggering rise in the family grocery bill. The cost of food is 20.9% higher in 2024 than it was in 2020. It is deeply concerning many people are using high APR credit cards to make ends meet.

Politicians who arrogantly dismiss pocketbook issues as no big deal ignore the reality that 81% of both Republican and Democratic voters named the economy as the top issue in the 2024 election.

For some, credit cards bridge a financial gap during an emergency. More than one-third of Americans (37%) cannot afford an unexpected expense over $400, and one-in-five (21%) have no emergency savings at all, reports financial services company Empower. Credit cards are the safety net for these people.

You can see where this is headed. The public is using credit cards at a higher rate today than ever before. They put their purchases on their credit card and will be faced with an exorbitant APR if their invoice is not paid-in-full each month. And there are a lot of purchases going on credit cards. According to Capital One, Americans “made an estimated $5.20 trillion in credit card purchases out of a total $8.29 trillion in 2023 retail spending.”

Yes, cash, debit cards, and digital wallets such as Apple Pay and Google Play are options for spending. But the amount of the purchase using those platforms is limited to what is in the buyer’s bank account.

Today’s credit card industry is not a free market. It is dominated by just a handful of players that behave in an anti-competitive manner. Visa and Mastercard are the most widely-used charge card processors. Nearly all bank cards (e.g. Capital One, Citi, JPMorgan, Bank of America) are associated with one or the other. The other credit card companies are Discover and American Express. That’s pretty much the lot.

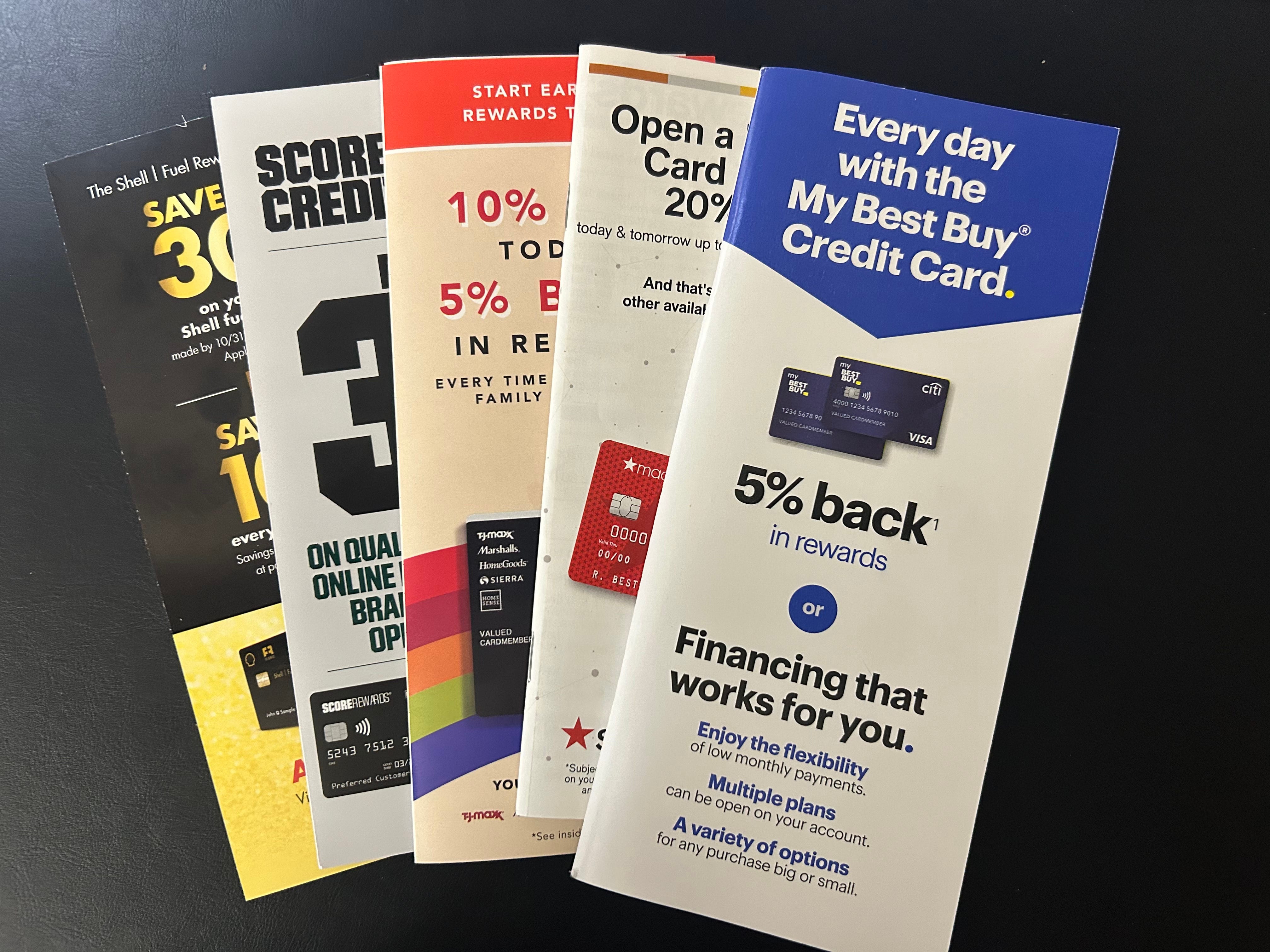

Retailers have gotten into the credit card business with store-branded credit cards. Some are closed-loop credit cards, meaning they can only be used with the issuing retailer. Others are open-loop credit cards, which may used anywhere that accepts the card’s brand, which is either Visa or Mastercard, in most cases.

Customers are enticed to apply for instant approval of a credit card at the check-out counter with attractive offers to save as much as 20% on that very purchase, and promises of savings on future purchases. It’s almost like getting free money, right? Realistically, it is not a whole lot different than dealer hooking a new drug addict.

Retailers do not actually issue or service the store-branded cards. That belongs to a third-party. Comenity Bank and Synchrony Bank are specialty banks that service hundreds of store-branded cards between the two of them. Joining them in backing retailer credit cards are American Express, Citi, JPMorgan, TD Bank, and a few others. In reality, there is very little competition.

Examples of cards include the Citi Bank-managed Home Depot credit card, a closed-loop card that may only be used at Home Depot stores. Its APR ranges between 17.99-29.99%, dependent on the applicant’s credit score. While the APR’s low range of 17.99% may appear steep, it is actually an outlier on the low side. Most credit card APRs are dramatically higher.

Examples of an open-loop credit card include United Airlines (APR 21.24%-28.24%) managed by JPMorgan, Shell (29.49%) operated by Citi, and the TD Bank-managed Target (29.95%). Some cards charge even higher interest rates with an APR above 30%. These include Dick’s Sporting Goods (31.74%) operated by Synchrony, Citi’s Best Buy (31.99%), Macy’s card from American Express (33.99%), and Synchrony’s TJX for TJ Maxx, Marshalls, HomeGoods, Sierra and Home Sense stores (34.99%). Because each of these cards are affiliated with Visa, Mastercard or American Express they can be used at any location that accepts those cards. This means more spending opportunities. And more high APR debt is likely.

The Federal Deposit Insurance Corporation reports the average annual interest rate earned on a savings account is just 0.43%. How can a bank charge a customer a credit card APR that is as much as 70-80 times the rate it pays that same customer on his savings?

There isn’t much serious competition because it’s difficult to get into the credit card business. During the mid-aughts, Walmart attempted to get in the banking business in order to issue its own credit card, among other services such as offering mortgages and opening savings accounts. A hailstorm by the financial industry and public officials erupted leading Walmart to abandon the plan. That the world’s largest retailer cannot offer competition to the credit card industry underscores the system is not operating in a free market.

If most credit cards are charging an APR in the 20-30% range then who is about to offer an APR in the single digits like, say 5.99%? There are no market incentives to do so.

Usury is defined as the practice of lending money at an exorbitant interest rate. If an APR of 34.99% does not constitute usury then what interest rate amount does? If gangsters were charging half that rate to loan money federal agents would be raiding their places of business.

Washington, DC policymakers should take steps to open the credit card industry to more competition and allow the free market to work to the benefit of the public.

Mark Hyman is a 35-year military veteran and an Emmy award-winning investigative journalist. Follow him on Twitter, Gettr, Parler, and Mastodon.world at @markhyman, and on Truth Social at @markhyman81.

His books Washington Babylon: From George Washington to Donald Trump, Scandals That Rocked the Nation and Pardongate: How Bill and Hillary Clinton and their Brothers Profited from Pardons are on sale now (here and here).